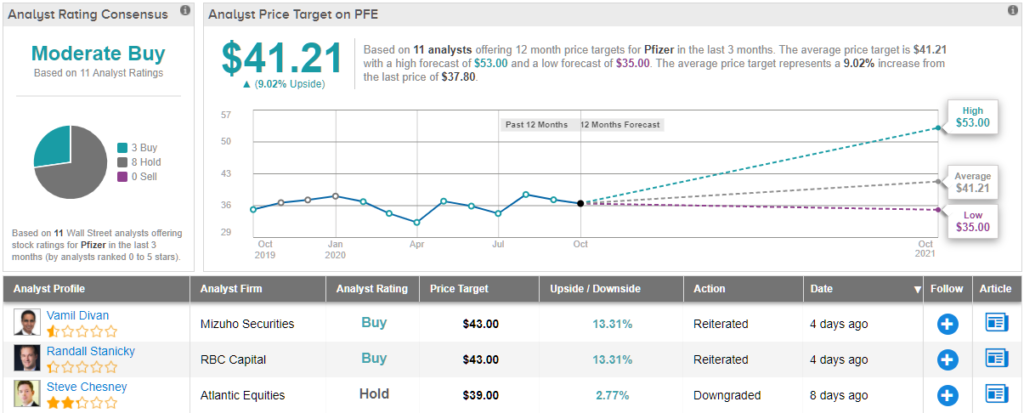

Overall, Divan has a Buy rating on PFE shares alongside a $43 price target.

Overall, based on 3 Buys and 8 Holds, the analyst consensus rates the stock a Moderate Buy.

With an average price target of $41.21, the analysts except shares to add 9% in the months ahead.

(See Pfizer stock analysis on TipRanks).

It could mark a shift in the weak diesel market that has benefited carriers and drivers for several months. Ultimately, the price of diesel will be set primarily by the price of crude.

But the spread between crude and diesel is also an important factor in the final pump price.

Diesel is a distillate; so is jet fuel.

But earlier this year, as diesel inventories began to soar due to changes being made by refiners seeking survival — more on that later — the days cover figure broke above 50 days.

A year ago at this time, it was 4.36 million b/d.Second, refiners made a lot less of it.

Last Friday, it settled at $43.32./bDuring that time, the front-month price of ultra low sulfur diesel on CME rose to $1.1791/gallon from $1.1598/g.

17.But by point of comparison, to show how much all that diesel inventory had held down prices relative to crude, the spread a year ago was about 53 cts/gallon. The current diesel to Brent spreads aren't sustainable.

If the move toward normalcy is going to start anytime soon, it could be that last week's numbers were the signal that it has begun.More articles by John KingstonGood news for diesel consumers, tough news for oil patch drivers in federal reportLabor Day, Roadcheck one-offs catch diesel traders by surpriseOOIDA scoffs at high cost estimates for broker transparencySee more from Benzinga * Options Trades For This Crazy Market: Get Benzinga Options to Follow High-Conviction Trade Ideas * FreightWaves CEO Interviewed On "The Business Of Content" Podcast * News Alert: US, Canada, Mexico Border Closures Extended To Nov.

While the overall market has recovered nicely from the pandemic swoon of mid-winter, many stocks are still struggling with a depressed share value.

Each is down at least 60% so far this year, but each also has a Strong Buy consensus rating and at least 40% upside potential for the coming months.Diamondback Energy (FANG)First up is Diamondback Energy, a Texas oil company that has been part of the Permian Basin boom which put Texas once again at the forefront of the North American oil industry.

While this number is up 40,000 barrels from the springtime, Diamondback has been hit hard by low oil prices in recent months and the stock is down 68% year-to-date.The low prices on the open oil market have impacted Diamondback’s bottom line, and earnings have been falling steadily from their $1.93 per share peak in 4Q19.

Given a focus on continuous cost reduction, we believe the company has the inventory depth and balance sheet strength to be a relative outperformer through the downturn,†Jayaram wrote.Jayaram rates FANG shares an Overweight (i.e. Buy), and his $48 price target suggests a 68% upside potential by next year.

(To watch Jayaram’s track record, click here)Overall, the Strong Buy consensus rating on FANG is based on 11 recent Buys against a single Hold.

The stock is selling for $28.58 per share, and its $52.10 average price target is even more bullish than Jayaram’s, implying an upside of 82%.

(See FANG stock analysis on TipRanks)ChampionX Corporation (CHX)Next up is ChampionX, an oilfield technology company acquired its current name this past summer, through the merger of Apergy Corporation and ChampionX Holdings.

He gives the stock a $12 price target, indicating confidence in 48% upside growth for the coming year.

(To watch Vaishnav’s track record, click here)Overall, CHX has 6 Buys and 1 Hold supporting its Strong Buy consensus rating.

With a bullish average price target of $14.09, Wall Street’s analysts see a 73% upside potential from the current share price of $8.11.

(See CHX stock analysis on TipRanks)Gol Linhas (GOL)From the oil industry, we move to the airline industry.

The difficulties facing the airline industry are apparent in GOL’s 62% share price decline since the start of the year.The hit Gol Linhas has taken is clear from the revenues and earnings.

"As we believe 2020 and 2021 will not be representative of GOL’s normal earnings potential, we are basing our 12-month PT on our 2022 forecast as GOL and the global airline industry begin to recover from the effects of COVID-19," the 5-star analyst noted.In line with this long-term optimism, Linenberg sets a $10 price target, implying an upside of 40% over the next 12 months.

(To watch Linenberg’s track record, click here)Wall Street agrees with Linenberg on the long-term potential here, and GOL’s Strong Buy consensus rating is based on a unanimous 5 Buys.

(See GOL stock analysis on TipRanks)To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.Disclaimer: The opinions expressed in this article are solely those of the featured analysts.

The deal would consolidate the NAND market, with Samsung, SK Hynix and Kioxia commanding more than 70% of revenue share, aiding NAND price recovery and narrowing losses, in our view.\- Anthea Lai, analystClick here for the research.The acquisition also further streamlines Intel’s struggling empire.

These tickers trading for less than $5 per share divide Wall Street like no other; market watchers either love them or hate them.It’s easy to understand the appeal.

On top of this, with shares changing hands for bargain prices, even what seems like miniscule share price appreciation can translate to monstruous percentage gains.

Calling Cotempla the “perfect complement to Adzenys,†he notes that each asset covers one half of the large stimulant market.The analyst added, “Adzenys XR-ODT has experienced impressive prescription growth over the course of the past year, and is now the preferred ADHD alternative dosage form taking over from Pfizer's market-leading Quillivant XR as its new-to-brand market share reached the number 1 position.â€Also promising, NEOS offers Adzenys ER, which is an extended-release liquid suspension stimulant product for ADHD.

Cacciatore points out that success with the liquid alternative dosage form has already been demonstrated as Pfizer’s Quillivant XR generated over $100 million in annual sales in 2017.To this end, Cacciatore rates NEOS an Outperform (i.e. Buy) along with an $8 price target.

Therefore, NEOS has a Strong Buy consensus rating.

At $8.33, the average price target is even more aggressive than Cacciatore’s and implies 1674% upside potential.

(See NEOS stock analysis on TipRanks)Dynavax Technologies (DVAX)Bringing extensive expertise in Toll-like Receptor (TLR) biology and cutting-edge adjuvant technology to the table, Dynavax develops vaccines to protect the population.

Thanks to its promising pipeline and $4.30 share price, Cowen believes investors should get in on the action.Representing the firm, 5-star analyst Phil Nadeau cites Heplisav as a key component of his bullish thesis.

Along with an Outperform (i.e. Buy) rating, he puts a $20 price target on the stock, indicating 370% upside potential.

3 Buys and no Holds or Sells add up to a Strong Buy consensus rating.

With an average price target of $16, the upside potential comes in at 276%.

(See DVAX stock analysis on TipRanks)La Jolla Pharmaceutical (LJPC)Last but not least we have La Jolla Pharmaceutical, which develops innovative therapies for life-threatening diseases with significant unmet need.

Given its impressive technology, Cowen sees its $4 share price as presenting an attractive entry point.Analyst Phil Nadeau, who also covers DVAX for the firm, highlights LJPC’s first commercial product, Giapreza, a patented formulation of the naturally occurring hormone peptide, angiotensin II, as a point of strength.

Even though the therapy’s utilization was most likely impacted by COVID-19, Nadeau has high hopes for the product.Nadeau argues LJPC will be able to leverage its existing infrastructure to market and promote Xerava, with only minimal additional spend expected.“Though Xerava has many competitors, the market for antibiotics used to treat intra-abdominal infections is large -- patients with appendicitis alone contribute to over 1 million hospital days each year in the U.S.

To this end, Nadeau projects $15 million in Xerava revenue in 2021, with this figure ramping to $60 million in 2024.Summing it all up, Nadeau stated, “Trading with a modest enterprise value, La Jolla is undervalued should Giapreza and Xerava be successfully commercialized.â€Taking the above into consideration, Nadeau rates LJPC an Outperform (i.e. Buy) rating along with a $20 price target.

Therefore, LJPC gets a Moderate Buy consensus rating.

Based on the $14 average price target, shares could skyrocket 251% in the next year.

(See LJPC stock analysis on TipRanks)To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.Disclaimer: The opinions expressed in this article are solely those of the featured analysts.

After charging off the starting line and posting huge market gains in 2020, recent events have put a halt to DraftKings’s (DKNG) spectacular debut as a publicly traded company.A recent share dilution, reports of new coronavirus infections in the NFL and in college football and this week’s lockup expiration (i.e. the end of the period when early investors and insiders are not allowed to sell shares into the market) – have all played their part in the stock declining by 30% since early October’s highs.But it has not all been bad news.

McTernan counts 3 reasons why the deal is a positive catalyst.For one, the analyst believes “Bleacher Report is an underrated sports media asset.†It is currently second only to ESPN in Instagram and Twitter followers and is the 22nd most used sports app in the iOS app store.Secondly, Turner “has strategic sports rights.†The analyst explained, "While the deal excludes NBA content given their existing partnership with FanDuel, Turner owns a portion of the rights for NCAA tournament games through 2032 and the MLB which Turner recently renewed through 2028."Lastly, media companies’ increasing acceptance of sports betting should “help grow market adoption and potentially legislation.†For example, TNT recently used TNT Bets in a simulcast of the NBA's Western Conference Finals playoff coverage, incorporating betting odds and analysis in its live stream.Now, following DraftKings’ latest announcement, the 5-star analyst notes, “All major sports media companies have a sports betting partnership.â€Overall, there’s no change to McTernan’s rating which stays a Buy, while the $65 price target stays put, too.

The stock has a Moderate Buy consensus rating based on 12 Buys and 6 Holds.

The forecast is for 28% upside in the year ahead, given the average price target clocks in at $57.35.

(See DraftKings stock analysis on TipRanks)To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.Disclaimer: The opinions expressed in this article are solely those of the featured analyst.

At some point over the next century, the stock market will lose more than 20% of its value in a single day.

stock market crash.